GMX's $GLP Wars: Pt. 2

GMX's $GLP Wars: Pt. 2

The war built around "real yield"

Welcome to Elaborate VC! This will be the second part of a two-part report about GMX that includes a summary of GMX’s functionalities and the protocols that are building on top of GMX and the GLP token, dubbed the “GLP Wars”. Read part one here.

Please share this newsletter if you think anyone else would benefit from reading it and feel free to share any thoughts with me about it via Twitter @Khrippex. Enjoy!

GLP

As a refresher on what the GLP token is, it is the liquidity provider token of the GMX platform. It consists of an index of assets that is used to swap with and trade against on GMX. It is broken down in a near 50/50 split between stablecoin assets and risk assets, primarily comprised of BTC, ETH, and USDC. The specific breakdown is in part one of this report here or can also be found here.

Traders on GMX trade against the GLP liquidity pool so the GLP pool makeup is always correlated with the amount of open interest per token on the platform at each time. For example, if a lot of traders are long ETH, then ETH would have a higher token weight in the pool, if a lot of traders are short, then a higher token weight will be given to stablecoins.

The GLP liquidity pool (which also refers to GLP token holders) is where 70% of revenue generated from the GMX platform goes to; this includes fees via liquidity providing and market making, swapping, asset rebalancing, and and most importantly, leverage trading (spreads, funding fees & liquidations). When traders losing money and/or get liquidated, the collateral is supplied to the GLP pool as profit and when traders profit, funds are paid out from the GLP pool. GLP holders essentially want traders to lose money on GMX because that is where their primary source of yield comes from.

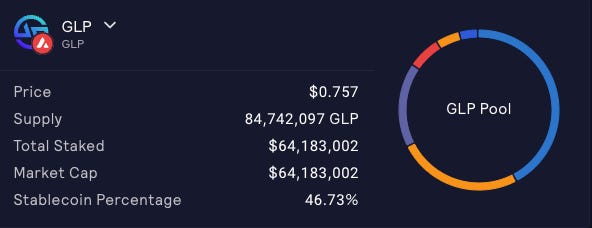

Price and Supply

As of writing, the price and supply of GLP on Arbitrum and Avalanche is as follows:

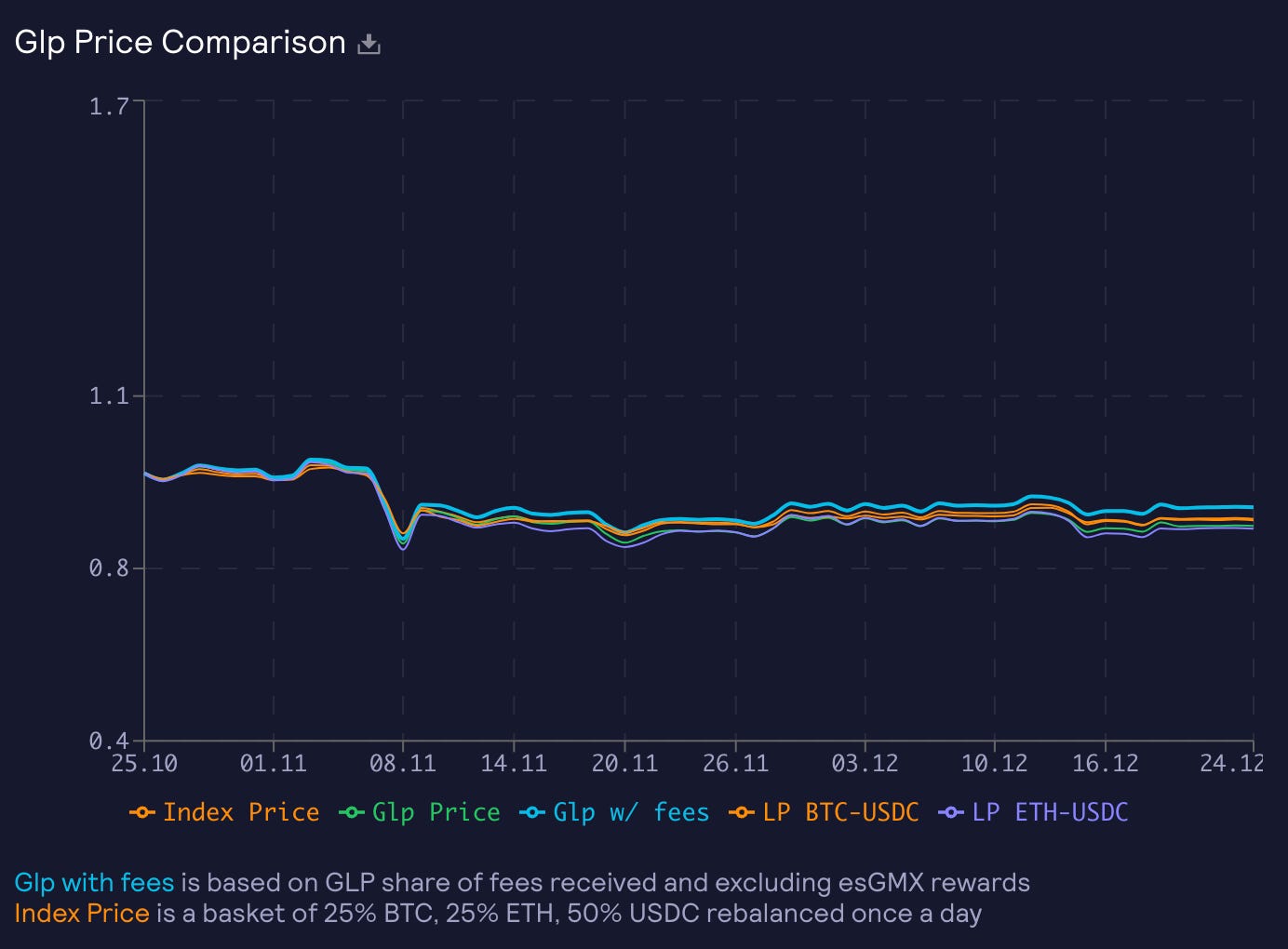

You can view the historical price performance of GLP here:

GLP Yield as a Building Block

GMX has been able to consistently attract traders and volume to its platform and thus, consistently generate fees and revenue for the platform, GLP token holders, and GMX stakers. Additionally, with GLP’s relatively stable price as a liquidity provider (LP) token that is not actively traded on exchanges and is backed by an index of assets, many community members see it as a prime asset to hold due to its relatively high and stable APR of 31.76% on Arbitrum and 36.15% on Avalanche.

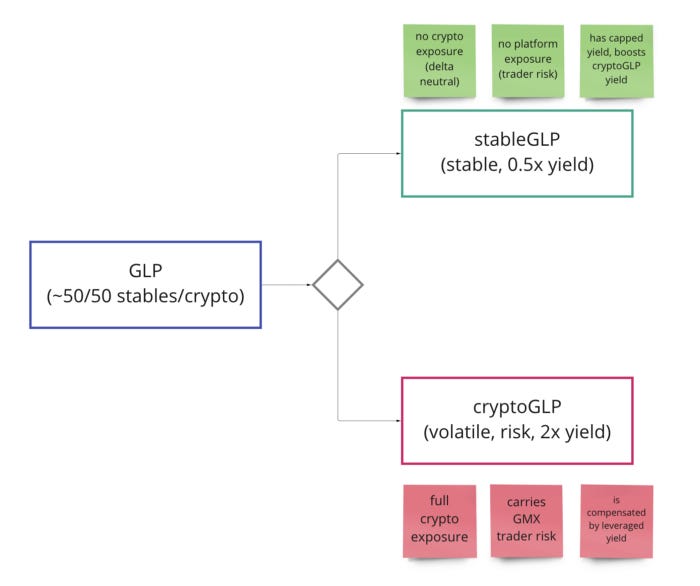

However, despite GLP’s relatively high and stable APR, there are numerous protocols out there building aggregators and vaults on top of it or trying to change or improve some intrinsic aspects of GLP like increasing leverage or minimizing price volatility to essentially go delta neutral. (Going delta neutral refers to Options Greeks where you can watch a video explanation by TD Ameritrade here and read specifically about what delta neutral means in the link provided.)

The “GLP Wars”

With the numerous attractive qualities of GLP as an asset like its ability to generate “real yield” through traders on the GMX platform and not token inflation, its relatively high and stable APR, its relatively well-balanced underlying basket of assets, all coupled with the meteoric growth of the GMX platform across the crypto industry, many are looking to capitalize. Some are looking to amplify their returns from GLP by introducing leverage while others are trying to minimize GLP’s price movements and claim “risk-free” yield through delta or gamma neutral strategies. However which way one is trying to build on top of GLP, it is clear that it has attracted numerous builders and traders, creating the so-called “GLP Wars” of protocols aiming to build the best and win the highest share of GLP tokens. This is similar to the “Curve Wars” and how protocols were attempting to win the highest share of CRV token deposits by building on top of Curve.

Rage Trade: Rage Trade focuses on ETH perps and delta neutral vaults based on GLP. Rage Trade describes their vaults as a way to “allow users to pool in funds for providing liquidity on GMX in a delta neutral way while earning ETH rewards on GMX”. Their vaults allow GLP holders to avoid some impermanent loss for a small decrease in APR by hedging their positions; they accomplish this by opening a short against the GLP position, so that any impermanent loss or gain would match profits or losses on the short, making the net position delta neutral, and earning a more stable APR.

Rage Trade currently operates two different vaults, Risk-Off Vault and Risk-On Vault:

Risk-Off Vault: When users deposit USDC into this vault, it lends the USDC to Aave and the Risk-On vault, earning interest from Aave and a fraction of ETH rewards from GLP based on the amount of USDC lent to the Risk-On Vault.

Source: docs.rage.trade/ylC5-mechanism Risk-On Vault: When users deposit funds into this vault, it provides a delta neutral GMX liquidity position by hedging GLP’s ETH & BTC price exposure based on their target weights by opening short positions on Aave and Uniswap. Although GLP has exposure to LINK and UNI on Arbitrum, it comprises 1.35% and 0.86%, respectively, so it is negligible. This vault is then able to provide an additional boost in yield by taking the escrowed GMX (esGMX) tokens, multiplier points, and ETH rewards received from holding GLP and auto-compounding ETH rewards into GLP along with restaking earned esGMX & multiplier points. You can read further into the vault’s hedging mechanism here and how it rebalances its portfolio here.

Jones DAO (JONES): Jones DAO is an options vault DeFi protocol that is aiming to build out two vaults based on GLP, jGLP and jUSDC. jGLP will be a leveraged GLP vault while jUSDC will be a vault to minimize price exposure, similar to Rage Trade’s Risk-On and Risk-Off vaults. They are going live on January 27, 2023.

jGLP: jGLP is a levered GLP vault that aims to use leverage to mimic the profile of the underlying assets of GLP, which are primarily BTC and ETC, so that users can gain exposure to BTC and ETH while collecting a multiplied level of GLP yield based on the leverage ratio.

jUSDC: jUSDC is a USDC vault that lends USDC to jGLP to allow for leveraging and in exchange, jUSDC collects a portion of the yield generated from the jGLP vault.

These two JonesDAO vaults operate within each other in a similar manner to the Rage Trade vaults that also lend and borrow from each other to minimize market exposure in one vault and maximize market exposure in another vault. You can read in-depth into both vaults in their whitepaper here, their “smoothpaper” here, or read @RealDegenGMX’s thread about the vaults here.

PlutusDAO (PLS): PlutusDAO is an Arbitrum-native governance aggregator that aims to attract user deposits of governance tokens and become a governance blackhole for projects with vested token structures. Currently, PlutusDAO supports Dopex, Jones DAO, GMX, and Sperax.

PlutusDAO aims to attract users to deposit their DPX, JONES, GLP, or SPA tokens into PlutusDAO so that PlutusDAO can aggregate tokens for governance power and to be able to provide deeper liquidity to liquidity pools to earn additional trading fees on top. In return, users who deposit their tokens receive plsAssets/plvAssets (plsDPX, plsJONES, plvGLP, plsSPA). These are essentially PlutusDAO’s liquid staking tokens that earn yield from the original protocol by having the underlying token locked as veJONES, veDPX, and veSPA, or held as GLP, and additional yield from PLS emissions from PlutusDAO.

As of writing, holding GLP tokens on Arbitrum currently earns the holder 31.85% APR but if users swapped their GLP for plvGLP and then staked it in PlutusDAO, they would be earning an estimated 37.45% APR instead, thus boosting their returns through PLS emissions while maintaining the same level of exposure to GLP. You can read about the specific mechanics relating to plvGLP here.

GMD Protocol (GMD): GMD Protocol is a yield optimizing and aggregating platform that currently provides single-sided staking vaults for BTC, ETH, and USDC that are built on top GLP. Users participate by staking their BTC, ETH, or USDC, with GMD and receive either gmdBTC, gmdETH, or gmdUSDC, based on which asset they staked. GMD Protocol then purchases GLP tokens with the assets received from stakers and redistributes half of the ETH rewards of GLP to stakers while the other half is distributed to GMD stakers.

Through GMD Protocol, users are able to gain access to half of GLP’s yield while maintaining exposure only to BTC, ETH, or USDC. Although it is impossible to perfectly hedge against the volatility of GLP and the broader crypto market, GMD Protocol employs a “pseudo-delta-neutral-strategy” to continuously rebalance their portfolio and make up any difference between deposited assets value and underlying GLP value in order to eliminate as much exposure to price volatility as possible. You can read more about the protocol here.

Neutra Finance (NEU): Neutra Finance is a yield optimizing platform that aims to provide “risk-hedged, sustainable investment strategies” through automated strategy vaults. Currently, Neutra Finance only has one product, their GLP Delta Neutral Vault, that was launched on January 20, 2023. The vault works by taking user’s deposited DAI and allocating about 90% of the DAI to buying GLP. The remaining 10% of deposits are used to open leveraged BTC and ETH shorts at around a 5.5-6x leverage point in order to allocate as much capital towards actually buying GLP while also remaining protected from the downside of GLP’s exposure to BTC and ETH. Neutra Finance then constantly rebalances the ratio between spot GLP exposure and leveraged short exposure based on liquidation risk and asset weight deviation with GLP’s underlying pool of assets. You can read a more in-depth overview here and learn about the specifics of the strategy here.

Neutra Finance is also looking to come out with additional products including other Delta Neutral Vaults for Sushiswap and Uniswap V3 to minimize the impacts of impermanent loss. They are also aiming to come out with an Automated 1x Bull Vault to allow users to gain exposure to the upside of an asset while earning yield on the asset with liquidation protection and a Uniswap V3 Automated Liquidity Manager so that liquidity provided to Uniswap V3 will be allocated at the optimal price range and automatically adjusted for changing price ranges.

DeCommas: DeCommas is a cross-chain DeFi automation layer protocol being developed under 3Commas, a centralized exchange. Although not yet out and aiming for a Q1 2023 launch date, DeCommas is working towards building a delta-neutral vault to earn yield while minimizing price exposure to the market.

You can read about the specifics here and their data testing done here.

Umami Finance (UMAMI): Umami Finance is a hybrid DeFi protocol that operates for centralized financial institutions. It aims to create “Non-Custodial, Institutional-Grade Investment Products for Core Crypto Assets” and then distributing them to the U.S. Institutional Market via Umami Advisors, its affiliated Registered Investment Advisor (RIA).

Umami Finance aims to launch various products in 2023 including UA DeFi Yield Indexes which is a curated index on “blue-chip” DeFi Yield strategies, an Institutional ETH Staking Pool to onramp institutional capital to an ETH Staking Pool build via a proprietary tech stack on Ethereum, and a Core Crypto Market-Maker that maximizes risk-adjusted returns on a dynamic index of Core Crypto assets by providing liquidity for a proprietary on-chain market-maker.

However, the first product that Umami Finance is working on is a Delta Neutral GLP Vault that generates returns on user deposited BTC, ETH, and USDC through GLP. Umami Finance’s vaults operate similarly to Neutra Finance’s vault where GLP APR is slightly reduced by their vault in return for hedging costs that minimize Delta exposure. Although their vault is not currently live yet, their strategy will include 5 GLP Vaults (USDC, BTC, ETH, UNI and LINK) that internally net Delta exposure to minimize hedging costs and maximize TVL allocated to GLP. You can read about the specific mechanics and back-tested data about their vault here and here or read @0xMedivh’s thread about it here.

Vesta Finance (VST): Vesta Finance is an over-collateralized debt lending protocol that operates similarly to MakerDAO. On September 13, 2022, Vesta Finance released a GLP vault that allows users to maximize their yield by applying leverage through lending. Vesta Finance users can collateralize their GLP tokens with Vesta Finance to mint VST tokens and increase their exposure to other yield-generating opportunities. For example, Vesta Finance proposes an option where users can collateralize GLP to mint VST and then stake the VST in a VST-FRAX stablecoin pool to generate additional yield with no additional price exposure. However, for true degens, users can also take their newly minted VST to buy more GLP, collateralize it, mint more VST to buy GLP with, and continue this cycle to maximize leverage. Read more about the specific mechanics here.

Dopex (DPX): Dopex is a decentralized options vault exchange that is integrating Atlantic Options with GLP to give users the ability to lever their positions. By using Dopex Atlantic Options, users can buy out of the money (OTM) GLP Atlantic Puts and borrow underlying stablecoins to purchase $GLP which is then staked to earn its share of protocol revenue. In doing so, users can hedge against GLP price action through Atlantic Puts. If the price decreases below the strike price, users earn the difference in settlement fees. If the price of $GLP goes up, users maintain their price exposure to $GLP and pocket the capital gain. You can read about the specifics here.

/ Twitter")

Unstoppable DeFi: Unstoppable DeFi is a protocol that aims to build a aggregated decentralized exchange through liquidity sourced from Uniswap, Sushiswap, GMX, and others. Although that product is still in development, they released the Unstoppable GLP Autocompounder on September 27, 2022, to automatically stack users’ GLP rewards for maximized APY. Before, the only way to compound GLP returns was to claim your rewards regularly on the GMX dApp, receive ETH to your wallet and then buy more GLP with it. With Unstoppable DeFi’s Autocompounder, users can deposit their GLP into Unstoppable DeFi’s vault which constantly harvests all of the ETH yield to mint additional GLP. It’s also free to use, meaning there are no fees collected by Unstoppable Finance for using the Autocompounder (this doesn’t mean you don’t have to pay blockchain transaction fees though).

On October 24, 2022, Unstoppable Finance came out with another product built on top of GLP, TriGLP, which aims to separate exposure to GLP into stable assets and volatile assets. Since GLP’s underlying basket of assets is approximately 50% stablecoins and 50% ETH/BTC, Unstoppable Finance thought it would interesting to tokenize each component to split the yield between the two in a way that is attractive for both and reflects the underlying risks.

Using this model and an assumption that GLP pays out ~20% APR, (it’s actually over 30% APR right now) Unstoppable Finance can create a delta neutral stablecoin-like position on one side with little market exposure earning ~10% APR and while keeping a position exposed to the market on the other side earning ~30% APR while maintaining full BTC and ETH exposure. You can read about the specific mechanisms here.

Mugen Finance (MGN): Mugen Finance is a multi-chain yield aggregator protocol built on top of LayerZero that uses protocols with sustainable models to generate yield. Currently, Mugen Finance only has one actively running strategy which is the GMX strategy. The GMX strategy takes USDC deposited by users and essentially dollar-cost-averages (DCA) into GLP. Future developments may make depositing into Mugen more attractive but as of writing, it would simply be easier and most likely more profitable to buy GLP directly from GMX without any additional fees. You can read about the specifics here.

Evidently, there are already several protocols that are building or have already built various different products and strategies on top of GMX’s GLP token and there will probably be several more as the market matures. GMX and GLP will be especially interesting to keep an eye on as it continues to sustain its trading fees and “real yield”.

To learn more about GLP and the GLP Wars, I’d recommend reading @defi_mochi’s Twitter thread here and here. @defi_mochi’s threads also contain information Dune dashboards that visualize much of the action going on in the GLP Wars.

I am not a financial advisor. The Content is for informational purposes only, you should not construe any such information or other material as legal, tax, investment, financial, or other advice.