DVT: SSV Network, Obol Network, Diva Protocol

DVT: SSV Network, Obol Network, Diva Protocol

Part 2

Welcome to my blog! After reviewing what Distributed Validator Technology (DVT) is, how it works, and why it’s important in part one of this report here, today I will be diving into the three protocols currently leading the charge on developing DVT. SSV Network ($SSV), Obol Network, and Diva Protocol, are each building and implementing DVT for the Ethereum network in their own separate ways, all of which I will review here.

Please share this newsletter if you think anyone else would benefit from reading it and feel free to share any thoughts with me about it at my Twitter @Khrippex. Enjoy!

Statistics:

Total Funding: $10M

Stage: Unknown

Investors: DAO Partner Program (Coinbase, Digital Currency Group, Gate.io Ventures, OKEx Ventures, Lead Capital, AMBER, Everstake, DappNode, and Valid Blocks)1

Current Team Size: 17

Location: Tel Aviv-yafo, Tel Aviv, Israel

Website: ssv.network

Background

SSV Networks was the first protocol to begin the development of Distributed Validator Technology (DVT) with the Ethereum Foundation (EF) after Ethereum developers realized how vulnerable single validators could be. During the genesis of the Ethereum Beacon Chain, Ethereum developers were running a validator for the Ethereum 2.0 testnet before experiencing downtime due to a hardware failure, prompting them to develop SSV (Secret Shared Validators), later renamed DVT, as a proof-of-concept. You can view the plan for SSV/DVT in Vitalik Buterin’s Ethereum roadmap below:

Ever since the proof-of-concept was developed for SSV/DVT back in 2020, Blox Staking, the organization developing SSV Network, began developing the technology after receiving a grant from the Ethereum Foundation in Q1 2020.2

Since then, SSV Network has released their own native utility token $SSV, “upgrading'“ it from Blox Staking’s native $CDT token, and launching DVT on testnet.3 SSV Network's most recent update was on March 30, 2023, announcing the launch of JATO, the most recent and last iteration of their public testnet before mainnet is finally launched.

Overview

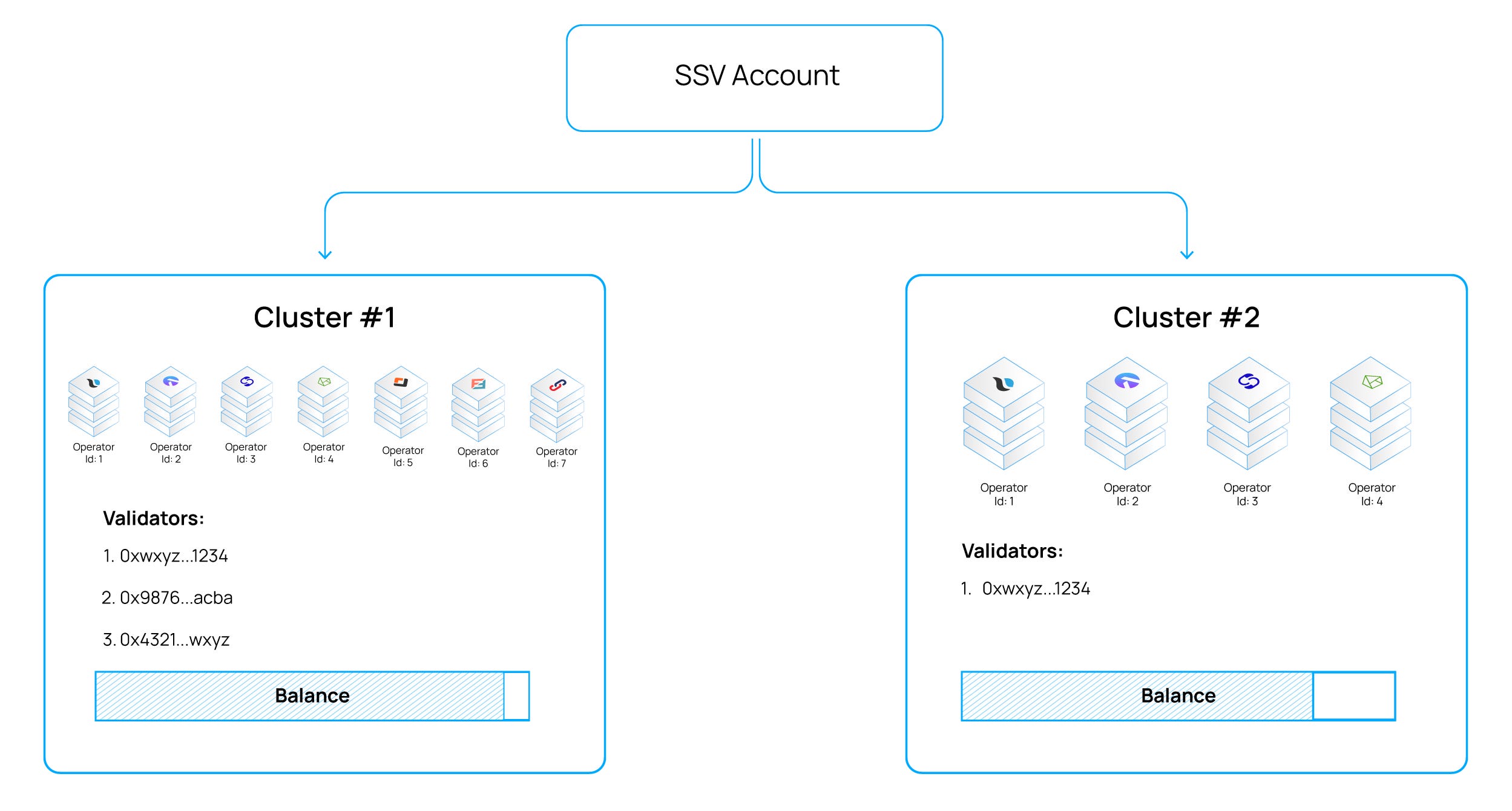

As stated above and explained in part one of this report, SSV Network aims to research and develop Distributed Validator Technology for Ethereum. SSV will provide the entire middle layer infrastructure to operate which includes staking pool smart contracts, registered validators, and operators to run all validators.

Through SSV Network, users who want to run their own distributed validator must select a cluster of operators from SSV Network in which to run their own validator before splitting the validator keys and registering the validator to the network. When setting up a distributed validator through SSV Network, users are required to go through operators. Operators are entities that provide hardware infrastructure, run the SSV protocol, and are responsible for maintaining the overall health of SSV Network. Operators also determine their own fees and are compensated for their integral services to the network by operating and maintaining validators on-behalf of stakers through clusters, a group of various validators. As a result, SSV Network users get to choose which operators will manage their validator based on performance history and operating fees when setting up their validator.

Tokenomics

During the token conversion event from $CDT to $SSV, SSV Network set it at a 100 CDT: 1 SSV token ratio.4 After the conversion, $SSV tokens were designated as SSV Network's native utility token, serving as both a governance token to participate in the SSV Network DAO and as a payment method for stakers to compensate operators that manage their validators. Stakers that use SSV Network must pay operators who are running validators on SSV Network with $SSV tokens and receive $ETH staking rewards in return.5

However, there was no mention of how tokens were allocated by the SSV Network team and there is no hard-coded max cap of the $SSV token built into the contract.6 The current circulating and total supply of $SSV as of writing (May 17, 2023) is 7,085,672 and 11,076,871 $SSV.7 This implies a circulating supply market cap. of $153,464,998 and a fully diluted valuation (FDV) of $239,908,344.

Use Cases

With SSV Network’s DVT infrastructure and its imminent deployment to mainnet, it is the leading protocol in the space. With its launch, it will have multiple use cases improving Ethereum as a Proof-of-Stake network and the specific validator UI/UX. Some of its specific improvements to the validating UI/US and use cases for the network are as follows:

Staking Pools

Optimized Rewards: SSV provides fault tolerance, optimizing performance and minimizing slashing risks

Security: By distributing each validator’s private keys to an offline source, it mitigates single points of failures

Deployment: SSV provides its operators and network as a service so that it is quick and easy to set up and manage your validators

Customizability: SSV users can choose between network operators, optimizing for cost and performance

Operators

Operating validators on the SSV Network maintain all of the same benefits listed above in optimized rewards, security, and deployment. However, operating validators on SSV Network also provides the benefit of creating a new revenue stream through fees collected via the SSV token for maintaining validators on behalf of stakers.

Solo Stakers

Solo validators on the SSV Network also maintain all of the same benefits listed above in optimized rewards, security, deployment, and diversification.

Conclusion

SSV Network and its trailblazing development in DVT make it a very interesting protocol to keep an eye on, for its potential contribution to Ethereum and for its potential profitability through the $SSV token. Obol Network is its primary competitor and the protocol most frequently named alongside SSV Network but it does not have a token nor does it state that it has any plans to launch a token. As a result, with the compelling reasons to develop DVT stated primarily in part one of this report, its leading position in DVT, and the fact that it has a token, I would continue to keep my eye on SSV Network, especially as it comes closer and closer to the sunsetting of JATO and the sunrising of mainnet.

Statistics:

Total Funding: $18.65M ($6.15M Seed, $12.5m Series A)

Stage: Series A

Investors: Ethereal Ventures, Coinbase Ventures, Acrylic Capital, Pantera Capital, Archetype, Nascent, BlockTower, Placeholder, Spartan, IEX8

Current Team Size: 24

Location: Ottawa, Illinois

Website: obol.tech

Background

Obol Network was founded in April 2021 by Collin Myers, the former head of global product strategy at ConsenSys. This was announced to The Block along with a $6.15M seed funding round led by Ethereal Ventures with participation from Coinbase and Acrylic Capital, among others.9

Shortly after Ethereum completed The Merge on September 15, 2022, Obol Network announced the Genesis Event of their community on October 21, 2022, discussing all aspects of their protocol including investors, advisors, mission, next steps, etc.

Overview

Obol Network operates a little differently compared to SSV Network; SSV Networks runs its own network with operators that users have to run their validators through while Obol Network simply gives users the platform and tools to run distributed validators by themselves. Obol Network’s calls their platform “Charon”, a GoLang-based, HTTP middleware that enables any existing Ethereum validator clients to operate together as part of a distributed validator. A single Charon client connects a validating client and a beacon node while multiple Charon clients form a cluster to behave as a single unified proof-of-stake validator together.

Obol Network launched the Obol Operator Community (OOC) on July 13, 2022, in connection with its first public testnet, Athena, from August 15-19, 2022. The first collaborative task was to begin testing the Charon client and it was deemed a success on August 22, 2023, with 5000+ signups, 200+ successful Distributed Key Generation (DKG) ceremonies, and 100+ Distributed Validator Clusters signing attestations across 40+ countries.

The next initiative announced on January 30, 2023, was the Bia Testnet and the Obol Ambassador Program, the second official testnet and an active program to help scale the project and increase awareness, respectively. Athena’s purpose to verify that DVT could enable better validator resiliency (and performance) while also improving operator decentralization while Bia’s purpose is to test DVT at a larger scale and test the DV Launchpad by enabling the community to configure Ethereum validator clusters through a web-based user flow.10 DV Launchpad is simply a website that allows groups of users to come together and create Ethereum validator threshold keys through a UI/UX friendly method.

Shortly after announcing Bia and the ambassador program, Obol Network announced Ethereum mainnet’s first distributed validator on February 22, 2023, with a roadmap of the protocol:

Obol Network’s most recent announcement was on April 17, 2021, announcing the conclusion of Bia Testnet and launching the Alpha Release of the Obol Network, deploying Ethereum mainnet distributed validators with the community for the first time.

Tokenomics

As of writing, Obol Network has not released any public details regarding a specific native token with no plans of releasing one either. In their docs, their response to “Does Obol have a token?” is “No. Distributed validators only use Ether”.

Conclusion

Obol Network’s platform will provide DVT across Ethereum’s staking landscape, providing many of the similar benefits that SSV Network’s DVT platform will to Ethereum. However, I believe Obol Network will be slightly more decentralized than their fiercest competitor, SSV Network, as they simply provide the infrastructure to spin up distributed validators. In order to run the Charon client and manage a distributed validator, users must still maintain their own hardware requirements on their own managed devices. On the other hand, SSV Network provides the entire network along with operators that manage the hardware for the validators in the network, posing structural issues that could more easily lead to levels of centralization amongst distributed validators.

I think the tradeoff that so many crypto protocols find themselves paralyzed in is present here; whether or not to make it more decentralized but harder to participate in for the community, or make it easier for users to sign up and join but as a result, create a more centralized structure. Obol Network seems to choose the prior while SSV Network seems to choose the latter. In this case, when speaking in terms of growth and price impact, especially considering the fact that Obol Network has no token and does not seem to have any plans for one, SSV Network shows capabilities of higher user growth and market share as well as an infinite amount of price action over Obol Network.

Statistics:

Total Funding: $3.5M

Stage: Seed

Investors: A&T Capital, Alphemy Capital, Gnosis, DCV Capital, Very Early Ventures, OKX, MetaWeb Ventures, Staked.VC, Bankless

Current Team Size: 8

Location: Unknown

Website: divalabs.org

Overview

Currently, Diva is not as comparable to SSV Network or Obol Network as it is comparable to a protocol like Lido. Right now, Diva’s main focus is to become a liquid staking protocol that aims to have all of its operators run distributed validator clients via Diva. Only in its future roadmap, does Diva have plans to allow anyone to run a node through its DVT network. As a result, Diva Protocol is more so in direct competition with Lido, Ethereum’s largest liquid staking protocol, as Lido has also been testing the application of DVT for their validators, mentioned in the last section of the first part of this report.

Despite Diva’s focus in liquid staking rather than providing DVT to node operators, I thought that they should be an honorable mention because Diva aims to use DVT for its network of validators and has ultimate goals to provide a similar platform to SSV Network or Obol Network where anyone could spin up a distributed validator through its own network. At launch, Diva would still provide the same benefits to validators operating on its network, similar to SSV Network, but it would just adopt a liquid staking protocol model like Lido.

Tokenomics

Diva currently has no mention of a native utility or governance token. It’s only token is its liquid staking token, divETH, that users receive 1:1 in return for depositing ETH with Diva.

Diva aims to launch wdivETH soon, a wrapped version of divETH that appreciates against ETH over time. When a user wraps one divETH into one wdivETH, the user will always have one wdivETH in its wallet even as it accrues staking rewards, meaning that as rewards are compounded, one wdivETH is simply backed by and worth 1.05 ETH, and then 1.1 ETH, and so on, as rewards are collected.11

Conclusion

Diva faces fierce competition from Lido as they both seem to be racing towards a liquid staking protocol model with the integration of DVT. However. Diva faces a giant in Lido with 31.18% of all ETH staked in the network being done through Lido as of writing on May 17, 2023.12 That figure currently sits at 6,274,784 ETH staked through Lido, magnitudes larger than even the second largest staking entity, Coinbase, with 11.2% marketshare and 2,254,784 ETH staked. However, I do think that if Diva can reach mainnet first and provide a significantly better staking product and thus, producing a much higher APR for staking with them compared to staking with Lido due to higher levels of validator resiliency, I could see some users migrate and Diva begin to steal market share, especially now that Lido V2 launched with 1:1 ETH:stETH withdrawals enabled. Getting to market first is one of the only viable paths I see for Diva to survive, even if it will remain in the shadow of Lido and DVT provides like SSV Network and Obol Network. Despite this belief, I think they are an interesting protocol to keep an eye on as they continue developing DVT for liquid staking.

To learn more about what DVT is and for some more in-depth reading, I’d take a look at Panther Academy’s article here, @Leo_Glisic’s Twitter thread here, Mara Schmiedt’s article here, and Chainslab’s article here.

I am not a financial advisor. The Content is for informational purposes only, you should not construe any such information or other material as legal, tax, investment, financial, or other advice.